Indonesia’s Central Statistics Agency (BPS) reported that the Indonesian economy grew by 5.11% in 2025, marking an improvement compared to the previous year. This growth was mainly supported by household consumption, stronger non-oil and gas exports, and resilient investment activity.

At the same time, Indonesia experienced a rare phenomenon: an annual deflation of -0.09% in February 2025, driven by declines in electricity tariffs and other government-controlled prices. Core inflation remained within Bank Indonesia’s target range.

The trade balance continued to record a substantial surplus throughout early 2025, reflecting Indonesia’s strong export performance, despite declining prices of key commodities such as coal. Bank Indonesia also maintained its benchmark interest rate at 4.75% throughout most of the year to help balance rupiah stability and ongoing economic recovery.

However, behind these stable macroeconomic indicators, businesses faced a different reality. The rupiah weakened and fluctuated between IDR 16,200–16,700 per USD, global demand remained unpredictable, and production costs continued rising—particularly in labor‑intensive industries. As a result, 2025 became one of the most dynamic and challenging years for Indonesian enterprises.

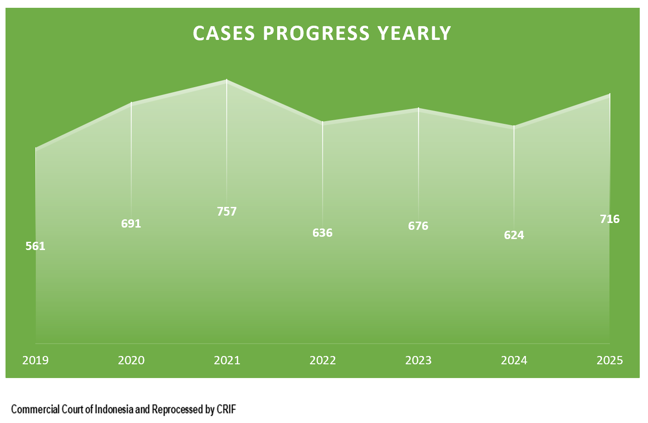

Although the national economy showed resilience—positive growth, manageable inflation, and persistent trade surpluses—many industries struggled with liquidity pressures, exchange‑rate volatility, and normalizing commodity prices. This situation was clearly reflected in the sharp increase in PKPU (Suspension of Debt Payment Obligation) cases, which rose to 716 cases in 2025, up from 624 cases in 2024.

The number of PKPU cases between 2019 and 2025 followed a fluctuating pattern. After peaking at 757 cases in 2021, the number declined in the following years before surging again in 2025. This trend aligned with early signs of a gradual recovery in the manufacturing sector. According to S&P Global, Indonesia’s Manufacturing PMI (Purchasing Managers' Index) improved from 50.4 in September 2025 to 51.2 in October 2025, indicating the beginning of production stabilization.

Companies also faced significant pressure due to the weakening rupiah and rising input costs. These conditions made it difficult for businesses—especially those highly dependent on export revenues or project cash flows—to meet their debt obligations, contributing to an increase in PKPU filings.

CRIF Indonesia assessed that the rise in PKPU cases in 2025 was primarily driven by the maturity of debts restructured during the 2020–2021 pandemic period. As repayment schedules fell due in 2025, many businesses found that their post‑pandemic recovery had not progressed as expected, prompting them to pursue PKPU as a mechanism to renegotiate debt terms such as tenor extensions or payment adjustments.

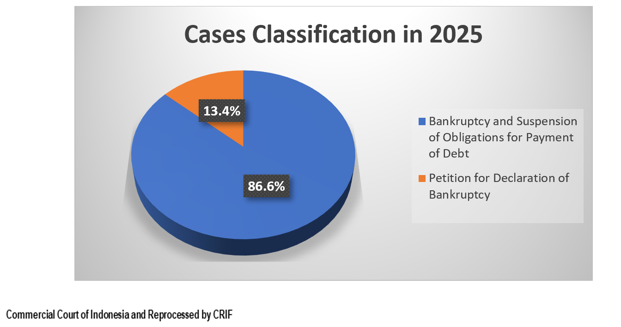

In 2025, approximately 86.6% of cases were related to PKPU or bankruptcy proceedings, while only 13.4% were pure bankruptcy filings. This indicates that financially distressed companies generally preferred renegotiation over liquidation. Stable monetary conditions—such as the steady BI rate and low core inflation—also supported this preference by giving debtors and creditors more room to negotiate.

Why PKPU Cases Increased in 2025?

The rise in PKPU cases did not occur overnight. Several interconnected factors pushed companies into the suspension-of-obligation process:

1. Maturity of Pandemic-Era Restructured Debts (“Maturity Wall”)

During the pandemic, many companies restructured or postponed debt payments. The impact appeared in 2025 when the new repayment schedules began to mature. Business recovery, however, remained uneven.

2. Rupiah Volatility

The fluctuating and generally weak rupiah impacted companies with USD‑denominated costs or debt, especially those dependent on imported components.

3. Declining Coal Prices

The downward trend in the benchmark coal price (HBA) reduced revenues across the mining sector, making it harder for companies to comply with loan covenants and finance operations.

4. Rising Layoffs

More than 42,000 layoffs occurred during January–June 2025, primarily in labor‑intensive sectors such as manufacturing and wholesale trade. Large-scale layoffs are often a signal of deep financial stress.

5. Construction Project Disputes

Large infrastructure projects often face delays, design changes, and payment discrepancies. These issues disrupt cash flows and remain a leading cause of PKPU filings in the construction sector.

Together, these five dynamics severely impacted companies’ liquidity stability, prompting many debtors to use PKPU as a survival and restructuring mechanism.

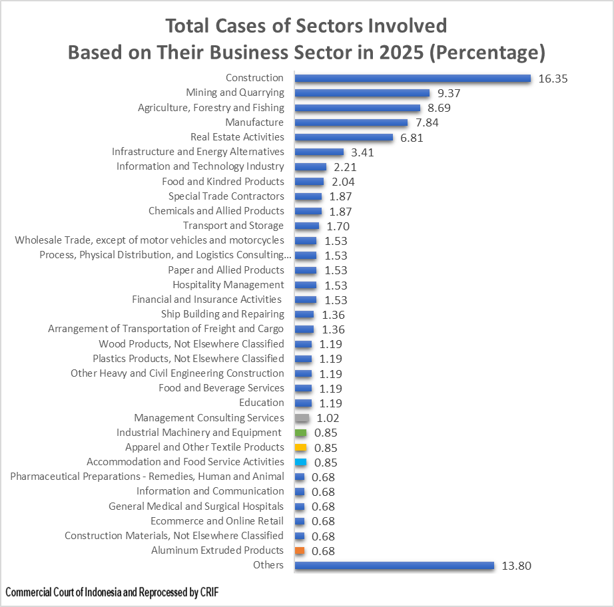

Sectors Most Vulnerable to PKPU and Bankruptcy

Analysis of PKPU cases indicated that certain sectors were more exposed than others:

Construction (16.35%)

As the sector with the highest share of PKPU cases, construction is extremely sensitive to payment delays, project disputes, and material price fluctuations.

Mining (9.37%)

Declining coal prices pressured revenues across mining companies and their related ecosystems such as contractors and logistics providers.

Agriculture, Forestry, and Fisheries (8.69%)

Weather volatility, price swings, and substantial working capital needs exposed this sector to financial instability.

Manufacturing (7.84%)

Labor intensive sub sectors—especially textiles, footwear, and electronics—were heavily affected by cheap imports, exchange rate pressures, and high production costs.

Property (6.81%)

Stable interest rates supported the market, but slow unit absorption and persistent construction expenses continued to pressure property developers.

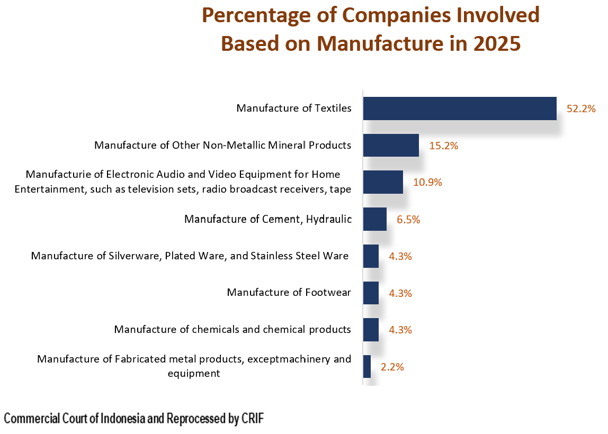

Which Manufacturing Subsectors Were Most Affected?

The manufacturing sector contributed significantly to PKPU cases in 2025. Among the subsectors:

- Textiles accounted for 52.2% of manufacturing-related PKPU cases, driven by weak export demand and competition from imports.

- The non-metallic mineral products subsector contributed 15.2%, reflecting its dependence on the property cycle.

- The audio-video electronics subsector (10.9%) was affected due to high import dependency and volatile component prices.

Several notable companies—such as Sritex, Asia Pacific Fibers, Sanken Indonesia, and Yamaha Music Products Asia—either entered PKPU or ceased operations, highlighting ongoing financial struggles in labor-intensive manufacturing.

While Indonesia’s PMI pointed toward modest recovery at the end of 2025, improvements were uneven, and many export-oriented manufacturers remained vulnerable to financial shocks.

PKPU Outlook for 2026: Stabilization or a another Wave?

Based on PKPU trends from 2019–2025 and supporting economic conditions, 2026 is projected to be a pivotal year. While some macro indicators point to stabilization, multiple dynamics may either improve or worsen PKPU numbers.

1. Macro Foundation for 2026: Stable, but Not Without Risks

Bank Indonesia projects Indonesia’s economic growth in 2026 to range between 4.9%–5.7%, supported by rising domestic demand and accommodative monetary policy. The BI Rate remained at 4.75% in early 2026 to maintain economic resilience and stability.

However, several risks remain:

- The rupiah continued to fluctuate, hovering near its weakest point due to global volatility and uncertainty in international financial markets.

- Inflation in February 2026 rose to 4.76%, indicating renewed price pressures compared to the deflation seen in 2025.

This suggests that although economic conditions are improving, 2026 also faces new pressures that could strain companies with sensitive cost structures.

2. The “Legacy of 2025”: Vulnerable Sectors Carry Over Their Problems

Several sectors that contributed heavily to PKPU cases in 2025, construction, mining, labor‑intensive manufacturing, and real estate, are likely to remain under pressure in 2026.

Construction: Recovery Held Back by Cash‑Flow Constraints

The construction sector continues to face persistent issues such as delayed payment terms, cost overruns, and project disputes. With a backlog of unresolved project problems and high dependence on external financing, cash‑flow pressures are expected to persist throughout 2026. These systemic challenges make the construction sector highly exposed to financial distress entering the new year.

Mining: Commodities No Longer a Strong Pillar

Coal prices trended downward throughout 2025, and global projections did not indicate a significant rebound in 2026. Mining companies that fail to adapt their business models away from commodity dependency may become the next group at risk of PKPU. The downstream impact is also expected to be felt by supporting industries such as mining contractors, logistics providers, and heavy‑equipment suppliers.

Labor‑Intensive Manufacturing: Still Fragile

The wave of bankruptcies among large manufacturers in 2025, including Sritex, Sanken, and Yamaha Music, illustrates that labor‑intensive industry players have not fully recovered. Global demand remains weak, while many companies still rely heavily on exports. Additionally, while the October 2025 PMI reached 51.2, signaling modest expansion, this improvement was not strong enough to protect vulnerable manufacturers from financial shocks.

Real Estate: Sensitive to Sales and Project Financing

Although stable interest rates may support the real estate market, unit absorption and buyer purchasing power are still limited. The sector remains exposed to financial risks, especially when sales fail to improve while developers continue to bear ongoing construction costs. This structural imbalance may continue to push real estate companies toward PKPU if market conditions do not improve meaningfully in 2026.

3. New Factors That Could Increase PKPU Cases in 2026

Rising Inflation

Higher inflation in early 2026 may squeeze profit margins, particularly for companies reliant on imported raw materials. As production costs rise while consumer purchasing power remains weak, liquidity pressures could intensify.

Increasing Debt Burden and the “Domino Effect of 2025”

Many companies survived 2025 only “half‑alive” by relying on internal restructuring or delaying payments. In 2026, short‑term debt coming due may overwhelm companies whose cash flows have not recovered as expected. This could cause a domino effect of distress, pushing more firms into PKPU.

Inconsistent Global Recovery

Export demand from the United States and Europe remains sluggish, putting sectors such as textiles, footwear, electronics, and automotive at continued risk. This aligns with the trend of factory closures and layoffs witnessed in 2025. Industries dependent on external markets could face additional stress if global economic recovery remains uneven.

4. Factors That Could Reduce PKPU Cases in 2026

Continued Investment Inflows

Investment realization reached IDR 1,714.2 trillion in 2024, and the positive trend could continue into 2026. New capital inflows could improve corporate liquidity and expand market opportunities for surviving businesses.

Manufacturing PMI Stabilizing in Expansion Territory

If the manufacturing PMI continues to hold above 50, this would indicate improving production activity and support a reduction in PKPU risk, particularly in non‑export‑dependent subsectors.

More Flexible Monetary and Fiscal Policies

Bank Indonesia has prepared a policy mix aimed at:

- stabilizing the exchange rate,

- stimulating credit growth, and

- expanding digital payment ecosystems.

These measures could provide additional breathing room for businesses facing liquidity challenges.

CRIF Indonesia assesses that 2026 will be a transition year, with PKPU trends highly dependent on how quickly vulnerable sectors—construction, mining, manufacturing, and real estate—adapt to lingering macroeconomic challenges.

Companies that proactively strengthen liquidity management, improve governance, and restructure early will be significantly better positioned to weather uncertainties compared to those that delay corrective action.

Conclusion

2025 revealed the widening gap between Indonesia’s stable macroeconomic environment and the financial reality faced by many businesses. While economic indicators pointed to resilience, pressures from currency fluctuations, rising costs, and maturing pandemic‑era debt caused corporate distress to spike.

As Indonesia moves through 2026, the trajectory of PKPU cases will serve as a key indicator of whether corporate recovery is taking hold—or whether economic pressures will trigger another wave of financial restructuring.

References:

BPS (Badan Pusat Statistik), CNBC Indonesia, Bank Indonesia (bi.go.id), S&P Global, PMI, CNN Indonesia, BeritaSatu, Bisnis Indonesia (ekonomi.bisnis.com), Satu Data Kemnaker (satudata.kemnaker.go.id), Trading Economics Kementerian Keuangan – BKF (fiskal.kemenkeu.go.id), Kementerian PUPR – Bina Konstruksi (binakonstruksi.pu.go.id)