At the close of 2025, Indonesia’s business landscape once again showed signs of turbulence. One of the clearest indicators was the rise in Suspension of Debt Payment Obligations (PKPU) cases—a legal mechanism used by companies facing liquidity pressures and needing temporary relief to restructure financial obligations.

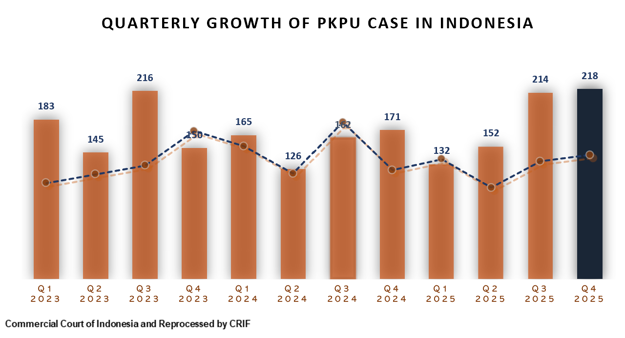

The economic landscape in Q4 2025 stood at a complex crossroads. On one hand, the post‑pandemic recovery continued to display elements of stability. On the other hand, structural pressures—including rising costs, currency volatility, weakened consumption, and tightened financing—continued to strain corporate liquidity. These pressures were reflected in the surge of PKPU cases, which reached 218 filings, the highest level recorded between 2023 and 2025. This article outlines the latest developments, the key factors behind this increase, and its implications for Indonesia’s business environment.

Data from the Commercial Court, reprocessed by CRIF Indonesia, show that Q4 2025 marked the most significant rise in PKPU cases over the past three years, with 218 cases, surpassing the 214 cases recorded in the previous quarter. Beyond statistics, this increase reflects growing financial pressure at year‑end—a period when businesses must meet targets, settle debts, and close financial books under volatile conditions.

This upward trend was not an isolated event. Throughout 2025, CRIF Indonesia recorded that PKPU and bankruptcy filings across the five major Commercial Courts increased by around 15% compared to 2024, indicating that many businesses were still undergoing consolidation after the pandemic and were facing prolonged liquidity stress. The spike in Q4 is therefore part of deeper, persistent economic dynamics observed throughout the year.

Meanwhile, global interest rates remained relatively high during 2025, pushing up corporate financing costs. This contributed to a recurring liquidity cycle in which revenue growth was insufficient, operating costs stayed elevated, and access to capital remained constrained.

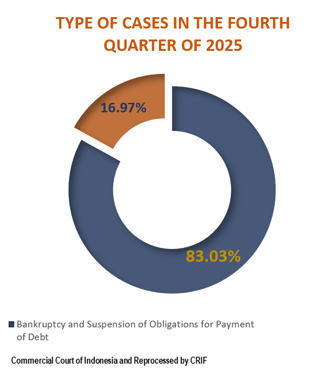

The dominance of PKPU, as reflected in the case composition for Q4 2025—with 83.03% PKPU cases and 16.97% bankruptcy petitions—suggests that most companies were seeking to survive rather than collapse. This aligns with global trends noted by UCC Global, where many jurisdictions in 2025–2026 adopted a “rescue over liquidation” approach, emphasizing restructuring as the preferred path. PKPU in Indonesia effectively pauses immediate financial pressure, creates space for renegotiating payment terms, prevents prolonged disputes with creditors, and helps sustain business operations.

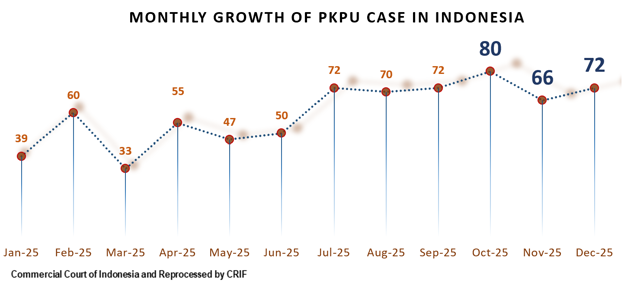

Monthly trends throughout 2025 show a clear pattern. Cases rose sharply from mid‑year onward, with the lowest point in March (33 cases) and the highest in October (80 cases). The October–December surge reflects typical year‑end liquidity constraints: increased inventory needs, short‑term debt rollovers in tight credit conditions, and heightened payment obligations. This pattern mirrors several high‑profile cases in 2025 involving major construction groups, state‑owned contractors, and manufacturing companies, highlighting sector‑wide liquidity compression.

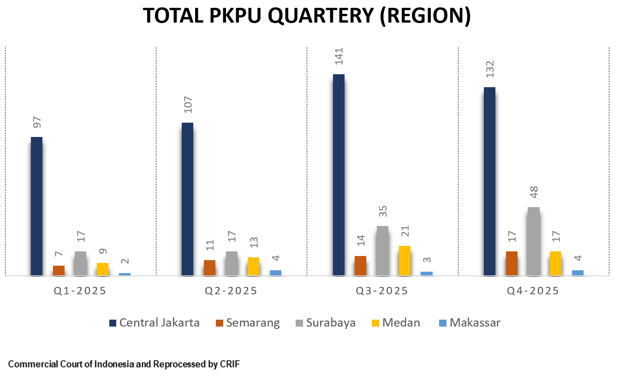

Regionally, PKPU cases were concentrated in Central Jakarta, which recorded 132 cases in Q4 2025. As the primary commercial hub and headquarters for many national corporations, the Jakarta Commercial Court naturally continues to receive the bulk of filings. However, another notable development was the sharp increase in Surabaya, which reached 48 cases in Q4. As the main industrial center of East Java, Surabaya faces additional challenges such as chronic congestion in industrial zones, inefficiencies in logistics infrastructure, and mobility constraints—all contributing to delays, margin pressure, and increased financial disputes.

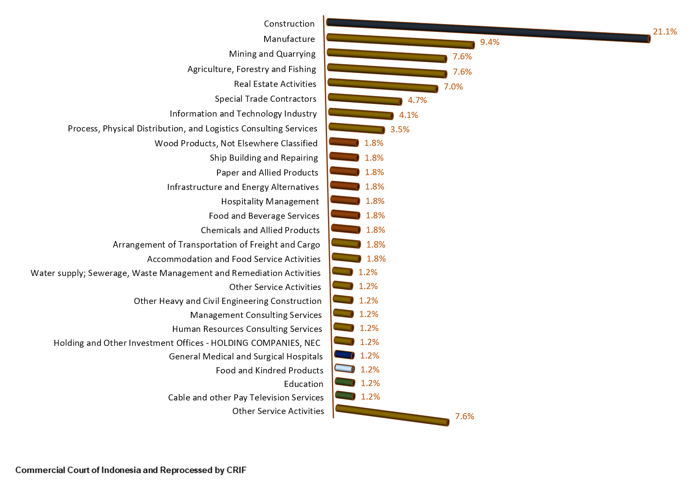

WHICH INDUSTRIES WERE MOST FREQUENTLY INVOLVED IN PKPU IN Q4 2025?

The construction sector accounted for 21.1% of PKPU cases in Q4 2025, making it the most vulnerable sector. This reflects the capital‑intensive nature of construction and its dependence on progressive project payments. According to reports from ANTARA and detikFinance, construction remains a strategic sector that employs more than 8.7 million workers and contributed 9.48% to national GDP in Q2 2025. However, delays in project disbursements, elevated financing costs, and postponed payments strained contractors’ cash flows, prompting more PKPU petitions. High‑profile cases involving subsidiaries of Wijaya Karya (WIKA) further underscored systemic pressures, even among state‑owned enterprises.

Beyond construction, the manufacturing, mining, and agriculture sectors also showed increased vulnerability in Q4 2025. Manufacturing faced rising input costs—particularly energy and imported raw materials—exacerbated by weakening global demand. Export‑oriented subsectors such as textiles and electronics were among those hardest hit. Mining and agriculture, meanwhile, faced commodity price fluctuations and seasonal impacts that disrupted cash flows and increased default risks.

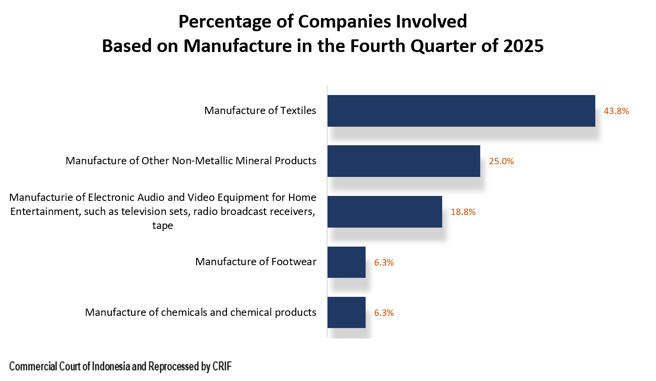

In manufacturing, the textile subsector faced the greatest strain, contributing 43.8% of PKPU cases within the sector in Q4 2025. Global uncertainty throughout 2025, especially among Indonesia’s key trading partners, reduced export orders for textile and garment producers. Reports also show declining demand, layoffs, and factory closures. CNBC Indonesia described the textile sector as approaching “sunset industry” status due to cheap import influxes, rising production costs, and persistent competitive disadvantages.

CHALLENGES & TRENDS OF PKPU IN INDONESIA’S MANUFACTURING SECTOR, Q4 2025

Entering Q4 2025, the manufacturing sector faced multidimensional pressures that contributed to rising PKPU cases.

The textile and textile products (TPT) industry experienced cheap import influxes, declining orders, low factory utilization, and excessive inventory buildup. These factors widened cash‑flow gaps and increased PKPU risk.

Exchange‑rate fluctuations and high energy prices increased production costs throughout 2025. Many manufacturers struggled with more expensive imported inputs, escalating energy bills, and rising borrowing costs—while selling prices could not keep up.

Banks became more selective in lending, especially to high‑risk sectors like textiles. Many companies struggled to access refinancing despite government support, forcing them to use PKPU to obtain temporary relief.

Supply chains had not fully normalized in 2025, causing unstable lead times for imported materials. Companies were forced to hold higher buffer stocks, tying up working capital and increasing liquidity pressure—particularly in capacity‑heavy industries such as textiles, electronics, and non‑metallic mineral products.

Conclusion and Solutions

Q4 2025 marked the peak of financial strain for many Indonesian companies. With 218 PKPU cases, the quarter recorded the highest level in three years. Yet the high proportion of PKPU relative to bankruptcy filings highlights a strong desire among businesses to survive through restructuring rather than closure.

Key insights include:

- Cash‑flow management remains the most critical factor for both large enterprises and SMEs.

- Q3 to Q4 represents a recurring vulnerability window due to seasonal financial pressures.

- Capital‑intensive sectors such as construction and manufacturing continue to face margin compression.

- Volatile financing conditions and exchange‑rate risks contribute to structural financial stress.

- Jakarta and Surabaya remain hotspots for commercial disputes and PKPU filings.

Practical Steps to Reduce PKPU Risk

1. Strengthen cash‑flow management

Improve receivables collection, accelerate incoming cash, renegotiate payment terms, and consider supply‑chain financing solutions.

Pursue refinancing early, maintain regular communication with creditors, and keep documentation well‑organized to support restructuring.

Streamline product portfolios, optimize suppliers, and adopt digital tools for inventory and production planning.

Diversify sales markets, use hedging to manage currency volatility, and conduct quarterly financial stress tests to assess resilience.

Together, these actions not only reduce PKPU risk but also build stronger financial structures, better governance, and more resilient operations in an increasingly unpredictable economic environment.

Reference:

[uccglobal.co.id], [antaranews.com], [finance.detik.com], [cnbcindonesia.com], [indotextiles.com], [ekonomi.bisnis.com], Commercial Court of Indonesia (Reprocessed by CRIF)